No. In most cases you can finance a foreclosure with a regular mortgage. The main exception is buying at a public auction, where cash is usually required.

Most investors treat “foreclosure” as one thing that always demands a briefcase of cash. It isn’t. It’s three different stages, and only one of them locks you out of financing. Get the stage right and you decide how the deal gets paid for: keep your cash, use a loan, or bring certified funds because the auction gives you no other choice.

Here’s how it breaks down, and where your capital actually has to show up.

Where your cash has to show up depends entirely on which stage of foreclosure you buy in.

In this guide:

- The Short Answer: No, Not Always

- Why the Answer Depends on the Foreclosure Stage

- Why Auctions Usually Require Cash

- How to Finance a Foreclosure Without Cash

- How Much Cash Do You Actually Need at Auction?

- Cash vs. Financing: Which Is Right for You?

- Common Mistakes to Avoid

- The Bottom Line

- Frequently Asked Questions

The Short Answer: No, Not Always

No, you don’t have to pay all cash for a foreclosure. Pre-foreclosures, short sales, and bank-owned (REO) homes can be bought with a regular mortgage, the same as any other house. All-cash is typically required only at the public foreclosure auction, where you have to settle in a day or two.

Financing a foreclosure isn’t the workaround. It’s the norm. Wells Fargo says approximately 60% of its foreclosed homes are purchased with financing (Policygenius). So the real question isn’t “cash or not.” It’s which stage you’re buying in, because that’s what sets the rule.

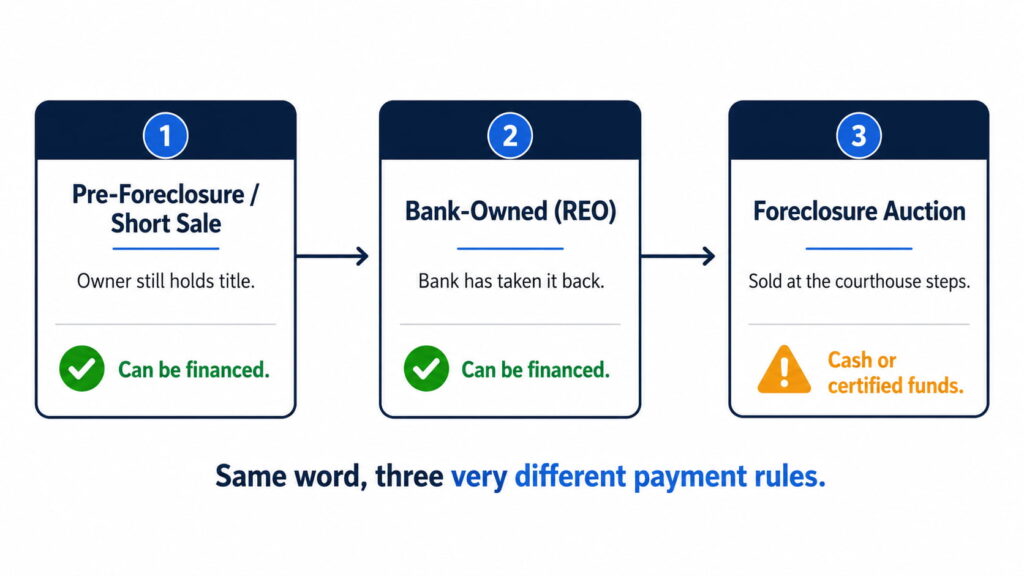

Why the Answer Depends on the Foreclosure Stage

“Foreclosure” covers three separate moments in the process, and each one has its own payment rule. Think of them as three different acquisition channels, each asking a different amount of capital up front.

One is the owner selling before the bank takes over. One is the bank selling after it took over. And one is the courthouse auction in between. You can finance the first two. The third is where cash lives.

Pre-Foreclosure and Short Sales

In pre-foreclosure, the owner still holds the title. They’re behind on payments and trying to sell before the bank takes the house. Sometimes they owe more than the home is worth, so the sale needs the lender to accept less than the full balance. That’s a short sale (Policygenius).

You can finance either one with a conventional or government-backed loan. There’s no cash requirement here. The catch is time, not money. A short sale can crawl, because the lender has to sign off on taking a loss, and that approval can drag on for months. So your constraint on these deals is patience and a rate lock that doesn’t expire, not a pile of certified funds.

Bank-Owned (REO) Properties

When a house doesn’t sell at auction, it reverts to the lender and becomes real-estate-owned, or REO. This is the most normal foreclosure to finance. If the home is livable, you buy it with a conventional, FHA, or VA loan like any other listing.

The wrinkle is condition. REOs sell as-is, and the appraisal can gate your loan. Banks won’t lend on a house with a hole in the roof or a missing furnace (Policygenius). Get preapproved before you make an offer. On an REO, a serious, financed buyer with paperwork ready beats a maybe every time.

Foreclosure Auctions

The auction is the cash exception. At a sheriff’s or trustee sale, you’re expected to bring cash or certified funds, close in roughly 24 to 72 hours, and you don’t get to inspect the property first (Auction.com).

That’s a different game with a different bankroll. It’s also why most operators shouldn’t start at the auction. The next two sections cover why the cash rule exists and exactly how much you need to show up with.

Why Auctions Usually Require Cash

This is the part most guides wave off. The auction isn’t cash-only because someone wants to keep you out. It’s cash-only because a mortgage physically can’t close that fast.

A lender won’t fund a loan without three things: an appraisal, an inspection, and a clear title. At auction, you get none of them. The property sells as-is, with no title report and no inspection period, so the buyer accepts whatever liens or problems come with it (Auction.com). No underwriter signs off on that.

Then there’s the clock. A normal mortgage takes about 30 to 45 days to underwrite (Rocket Mortgage). The auction gives you 24 to 72 hours to settle. Those two timelines don’t overlap, so the sale gets paid in certified funds.

A mortgage takes 30 to 45 days to underwrite. An auction gives you 24 to 72 hours to pay. That gap is the whole reason auctions are cash.

How to Finance a Foreclosure Without Cash

For the financeable stages, pre-foreclosure, short sales, and REO, you have four main routes. The point of financing isn’t just affording the house. It’s keeping your capital spread across more deals instead of sunk into one.

One heads-up before the list: two of these four are owner-occupant programs. FHA and the 203(k) are built for people who will live in the house, which makes them tools for a house-hack or a live-in flip, not a straight rental or a quick flip you never move into.

Conventional Loans

A conventional mortgage is the standard route for a livable REO or short sale. Step one is preapproval, which tells sellers and listing agents you can actually close. The home has to be in insurable, lendable condition, so anything structurally broken can stall the loan until it’s fixed.

If the foreclosure needs work but not a gut job, a renovation mortgage like Fannie Mae’s HomeStyle wraps the purchase price and the repairs into one loan. It generally wants a credit score around 620 and can go as low as 5% down (Policygenius).

FHA Loans (3.5% Down)

FHA is the low-cash path. You can put down as little as 3.5% with a credit score of 580 or higher, or 10% with a score between 500 and 579 (Rocket Mortgage).

Two conditions matter for a foreclosure. First, the home has to meet FHA minimum property standards: safe, structurally sound, and sanitary. As-is foreclosures often flunk that until repairs are made, which can hold up the loan. Second, FHA is for owner-occupants. It’s not meant for investors or house-flippers (Policygenius). If you plan to live in the property, it’s one of the cheapest ways in. If you don’t, skip to conventional or hard money.

FHA 203(k) Renovation Loans

The 203(k) is the standout for a beat-up foreclosure, because it finances the purchase and the repairs in a single loan. There are two versions. The Limited 203(k) lets you borrow up to $75,000 for non-structural work. The Standard 203(k) handles structural jobs, requires a minimum of $5,000 in repairs, and brings in a HUD consultant to oversee the project (Rocket Mortgage).

The rules are strict. A licensed contractor has to do the work, and it must start within 30 days of closing. Like standard FHA, the 203(k) is a primary-residence program, not an investment-property loan (Rocket Mortgage). For an operator willing to live in the deal while it’s rehabbed, it’s a way to buy and fix with very little cash. For a pure flip, it’s the wrong tool.

Hard Money and HELOCs

These are the investor’s real financing tools for foreclosures. Hard money is fast, short-term, and asset-based: private lenders care about the property’s value more than your credit, they can fund in a couple of days, and they’ll often want up to 30% down at higher rates and fees (Policygenius).

That speed is the move that gets you into an auction. Experienced investors close like cash with hard money, renovate, then refinance into a cheaper conventional loan once the property can pass a bank inspection. A HELOC does something different: it pulls equity out of a property you already own to fund the next one. Both work. Both cost more than a standard mortgage, so price the interest into the deal before you sign.

How Much Cash Do You Actually Need at Auction?

There’s no national number. Auction rules are set county by county, and they vary. But the shape is consistent: a deposit the day of the sale in certified funds, then the balance fast. Here’s what that looks like in three real jurisdictions.

In Philadelphia, you post a $5,000 deposit plus a $35 non-refundable fee just to bid. That deposit applies to a 10% down payment due by the next business day, with the remaining 90% due by the fifteenth day after the sale (Philadelphia Sheriff).

In Florida, the winning bidder owes 5% of the bid in certified funds immediately at the end of the sale, it’s nonrefundable, and the balance is due the same or next business day (Brevard County Clerk). In Lorain County, Ohio, win a $100,000 bid and you hand over a $5,000 cashier’s check on the spot, then bring the remaining $95,000 within 30 days. Miss that deadline and interest starts stacking at 10% a year (Policygenius).

The through-line: if you miss the balance deadline, you forfeit the deposit. Verify your own county’s rules before you raise your hand, because the number that matters is the one your courthouse prints, not the one in this article.

Cash vs. Financing: Which Is Right for You?

Cash and financing solve different problems. Cash buys speed, a stronger negotiating position, and access to auctions, but it sinks your capital into one property. Financing preserves your liquidity and lets you spread the same money across several deals as down payments, but it’s slower and the house has to qualify.

Run the math on your own capital. One all-cash purchase ties up, say, $150,000 in a single deal. The same $150,000 as 25% down covers three or four financed deals. Cash wins on speed and it’s the only way into most auctions. Financing wins on deal count.

| Factor | Cash | Financing |

|---|---|---|

| Speed to close | Days | ~30–45 days (longer for 203k) |

| Capital tied up | Full purchase price in one deal | Down payment only; rest spread across deals |

| Auction access | Yes | No |

| Negotiating power | Strongest (certain, fast close) | Weaker (contingent on approval and appraisal) |

| Condition limits | Buy anything, any condition | Home must meet lender/insurer standards |

| Best fit | Auction hunters, flippers who need speed | Buy-and-hold, portfolio builders |

Pick by your model. If you chase auctions and flips where speed wins the deal, cash (or hard money that acts like it) is your lane. If you’re building a rental portfolio, finance the financeable stages and keep your cash working. Either way, the real bottleneck usually isn’t capital. It’s deal flow. You still have to be the buyer a distressed seller finds first, which is exactly what organic motivated-seller leads are for.

Common Mistakes to Avoid

The difference between a foreclosure deal and a foreclosure trap is usually one of these:

- Assuming every foreclosure needs cash. You just talked yourself out of the roughly 90% you could have financed.

- Bidding at auction with no certified funds or inspection lined up. You’re buying blind, and if you win you can’t pay.

- Underestimating repairs. The “deal” evaporates the moment the real rehab number lands. Run it before you bid, not after.

- Skipping preapproval before you offer on an REO. Cash-flush investors take the property while you’re still filling out forms (Policygenius).

- Ignoring liens and back taxes. At auction there’s no title report, so unpaid liens can survive the sale (Auction.com). Win the bid, inherit the debt. This is the one that quietly wrecks new auction buyers.

The Bottom Line

So, do you have to buy a foreclosure with cash? Only at the auction. Pre-foreclosures, short sales, and bank-owned homes finance like any other purchase, and most foreclosures are actually bought with a loan. Match the stage you buy in to the money you have: finance what you can, reserve cash (or hard money that closes like it) for the auctions that demand it, and the “cash-only foreclosure” myth stops costing you deals.

Before You Chase Your Next Foreclosure Deal

Financing answers how you’ll pay for the next foreclosure. It says nothing about how a seller in trouble will find you first, and that’s the half most operators leave to luck. Building the organic lead channel that puts you in front of motivated sellers is what we do at BASEO, exclusively for cash home buyers.

If you want to see where your own site stands before your next deal, send your domain for a free, written audit: your three biggest issues, the local keywords your top competitor ranks for that you don’t, and the deal-math projection for your market. No call required, and it’s yours to keep.

Frequently Asked Questions

No. Most foreclosures, including pre-foreclosures, short sales, and bank-owned (REO) homes, can be purchased with a regular mortgage. All-cash is typically required only at public foreclosure auctions, where buyers must close within a day or two using certified funds.

Yes. Bank-owned (REO) and pre-foreclosure homes that are livable can be financed with conventional, FHA, or VA loans, just like any other property. The main catch is that the home must be in insurable condition to qualify for financing.

Auctions require winners to close in 24 to 72 hours, with no inspection or appraisal allowed beforehand. Mortgage lenders can’t underwrite a loan that fast or without a clear title, so sales are settled with cash or a cashier’s check instead.

Yes, if the home meets FHA minimum property standards and will be your primary residence. You can put down as little as 3.5% with a 580+ credit score. An FHA 203(k) loan can even bundle the purchase and renovation costs together.

It varies by county. Most require a deposit of about 5% to 10% of your bid (sometimes the full amount) the day of the sale via cashier’s check, with the balance due within 24 to 72 hours. Miss the deadline and you forfeit your deposit.