A house two streets over just got a Notice of Default. The owner still has the keys, still lives there, and still controls what happens next. For a few months, you can knock on that door and make a deal before the bank ever takes it to auction.

That window is pre-foreclosure. Here’s what it means when you’re the one buying, how the timeline works, how to actually close one, and the risks worth verifying first.

An investor sizing up a pre-foreclosure before it ever reaches the courthouse steps.

Pre-Foreclosure, Explained in One Minute

Pre-foreclosure is the window after a homeowner falls behind on mortgage payments and gets a Notice of Default, but before the bank sells the home at auction. For a buyer, it means you can negotiate directly with a motivated owner who still holds title, often below retail.

It doesn’t start on the first late payment. Under federal law, a lender generally can’t begin foreclosure until the borrower is more than 120 days delinquent (Nolo). A formal Notice of Default usually lands after roughly three missed payments, once the grace period and lender outreach have passed (Upsolve).

From there, the owner is in mortgage arrears but still owns the home. Pre-foreclosure ends one of three ways: the owner reinstates the loan and keeps the house, sells it (to you, if you move), or it goes to auction. You’re dealing with a person, not a bank.

What Pre-Foreclosure Means for You as a Buyer

For a buyer, pre-foreclosure is two things at once. It’s a real opportunity to buy below retail from a seller with a reason to move fast. It’s also a deal with more moving parts than a normal purchase, and a seller who can still change their mind. Both sides are worth understanding before you knock.

The Opportunity: Below-Market Price and Less Competition

The owner is motivated in a specific way: a completed foreclosure wrecks their credit for years, so many would rather sell and walk than let the bank take it. That motivation is where your room to negotiate comes from.

The homes are often in better shape than what you’d find at auction, because the owner still lives there. And many never hit the MLS. A pre-foreclosure isn’t automatically for sale (Zillow), which means less competition than the open market, where every listing draws a crowd. You’re working off public records, not a bidding war.

There’s usually a discount, but be honest about it. There’s no fixed number. What you save depends on the owner’s equity, the condition of the house, local demand, and how motivated the seller really is. Pre-foreclosures tend to sell for less of a discount than bank-owned or auction homes, precisely because the owner still controls the sale.

The channel isn’t small, either. ATTOM reported 118,727 U.S. properties with a foreclosure filing in the first quarter of 2026, up 26% year over year (ATTOM). More filings means more owners in that pre-auction window.

The Catch: A Motivated but Still-in-Control Seller

Here’s the friction. Until you have a signed contract, the owner is still in control. They can reinstate the loan, refinance, borrow from family, or work out a plan with the servicer, and your deal evaporates.

If the owner owes more than the house is worth, they’re underwater, and the sale can’t happen without the lender agreeing to take less than the balance. That’s a short sale, and it changes the math. A short sale needs the lender’s approval, and every lienholder has to sign off, not just the first mortgage. Junior lienholders, a second mortgage or an HOA, can refuse a deal that leaves them with nothing (Nolo).

That makes these deals run longer than a normal sale, and it puts you across the table from someone under real stress. Approach the conversation with tact. The investors who close pre-foreclosures consistently are the ones the seller trusts, not the ones who show up treating a hard moment like a fire sale.

Pre-Foreclosure vs. Foreclosure vs. Short Sale

Buyers mix these three up constantly, and the difference decides how you buy and how much diligence you get.

Pre-foreclosure means you buy directly from the owner, before the auction, while they still hold title. Foreclosure, once it’s complete, means the bank has taken the home; you buy it at the courthouse auction or later as an REO (real-estate-owned) listing from the bank, usually as-is and often with little time to inspect (Rocket Mortgage). A short sale is a way of selling, not a separate stage: the owner sells for less than they owe with the lender’s sign-off, and it typically happens during pre-foreclosure (Nolo).

| Pre-Foreclosure | Foreclosure / REO | Short Sale | |

|---|---|---|---|

| Who owns it | The homeowner | The bank / lender | The homeowner (still) |

| Where you buy | Directly from the owner | Auction or from the bank | From the owner, with lender sign-off |

| Buyer due-diligence time | More: you can inspect and pull title | Little: often as-is, sometimes sight-unseen | More, but slowed by the lender |

| Typical price vs retail | Some discount, varies | Often a larger discount | Below what’s owed, lender-approved |

Where you buy, and how much room you get to inspect, changes at every stage.

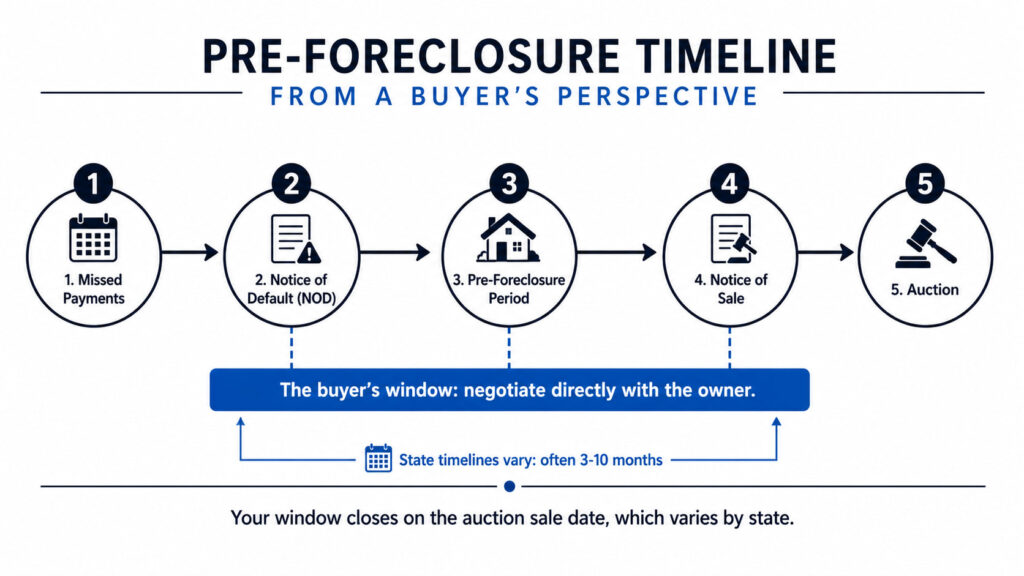

The Pre-Foreclosure Timeline (and Where Buyers Fit In)

The sequence is consistent even when the clock isn’t: missed payments, then a Notice of Default, then the pre-foreclosure period, then a Notice of Sale, then the auction. Your window is any point before that auction sale date.

The length of that window is where it gets local. Judicial-foreclosure states run the process through the courts, which is slower. Non-judicial states follow notice steps defined by statute and can move in about 120 days, sometimes longer (Nolo). California, for example, gives the owner 90 days from the recorded Notice of Default to cure before the process can advance (California Courts). Depending on the state, the whole run from default to auction often lands somewhere between three and ten months.

That variation matters for you. In some states an owner has as little as 30 days to actually close a pre-foreclosure sale before the bank takes over (Zillow). Before you invest time in a property, confirm the scheduled sale date and learn how your state handles the process, including any redemption period after a sale. That one check tells you how much runway you have.

Where a buyer fits: any point before the auction sale date, on a clock that varies by state.

How to Buy a Pre-Foreclosure Home, Step by Step

This is the part you came for. Here’s the sequence from finding a property to closing on it, in the order an operator actually works it.

1. Find Pre-Foreclosure Properties

Most pre-foreclosures aren’t sitting on the MLS waiting for an offer. You find them at the source:

- Zillow’s pre-foreclosure filter and similar portal filters

- County public records and Notice of Default filings, the raw feed

- RealtyTrac and Foreclosure.com, aggregated listings

- HomePath (Fannie Mae) and HomeSteps (Freddie Mac) for later-stage inventory

- Local legal-notice newspapers, where sale notices are published

- Driving for dollars and direct mail, working a target neighborhood

Those are all outbound: you chase the list, and so does every other investor with the same subscription. The source that compounds is inbound, being the site a distressed owner finds when they open their phone and search their exact situation. That’s the seller-situation search channel a specialist team like BASEO builds for cash home buyers, so the leads come to you instead of you buying the same NOD list as everyone else. If you want to see how that channel is built, start with SEO built for cash home buyers.

2. Research the Property, Loan Balance, and Liens

Before you talk price, pull the numbers. Find the outstanding loan balance, the payoff, because on a non-short-sale deal that’s your floor: the sale has to cover the debt.

Then check what else is attached to the title. A title search is the only reliable way to surface every lien on a property, second mortgages, HELOCs, IRS or property-tax liens, mechanic’s liens, unpaid HOA dues, and some of those survive a foreclosure and land on the next owner (New Funding Resources). Pull public records or open a file with a title company early. And confirm with the trustee that the property is genuinely still in default and not already reinstated or scheduled for sale sooner than you think.

3. Contact and Negotiate With the Homeowner

Reach the owner by mail or a respectful door-knock. Remember who’s on the other side: someone having a hard year, not a motivated seller in a marketing funnel. Lead with that.

The pitch is a real win-win. A completed foreclosure follows them for years; selling to you lets them walk away cleaner, and often with a little cash instead of none. On price, anchor to your numbers: ARV minus repairs minus the payoff and your margin. That’s the cash offer that has to work for you.

One hard constraint sits under every conversation. Unless the lender approves a short sale, the price has to at least satisfy the mortgage payoff. If the owner has equity, you have room. If they’re underwater, you’re not really negotiating with them anymore, you’re negotiating with the lender.

4. Make an Offer With the Right Contingencies

Put it in writing with a purchase agreement, drawn up by an agent or, better on a distressed deal, a real estate attorney. This isn’t the step to freelance.

Three contingencies protect you specifically here: a clear, marketable title (so you don’t inherit those liens), a professional inspection (so a hidden repair bill doesn’t erase your margin), and financing if you’re not paying all cash (SmartAsset). Distressed properties carry more title surprises and more deferred condition than a normal sale, so these contingencies are your exit if the diligence turns up something ugly.

5. Handle the Lender (Short Sale Approval)

If the home is worth less than the owner owes, the lender has to approve the short sale, and this is where deals stall. The lender isn’t obligated to say yes, and when there’s a second mortgage or other junior lien, every one of those lienholders has to sign off too. Any one of them can refuse (Nolo).

Plan for it to take weeks, sometimes months. What moves it along is clean paperwork, a complete package, and steady, professional communication with the loss-mitigation department. Patience is part of the acquisition cost on an underwater deal. If you can’t carry that uncertainty, target owners with equity instead.

6. Inspect, Title Search, and Close

Before money moves, do the two things auction buyers usually can’t. Inspect the property so you’re pricing real repairs, not guesses. And run a full title search so no surprise lien shows up after you own it.

Then close through a title or escrow company that handles the payoff and records the transfer cleanly. This is the quiet advantage of pre-foreclosure over the courthouse steps: you get real due-diligence time. At auction you often buy sight-unseen and inherit whatever’s on the title. Here, you get to look first.

Risks of Buying a Pre-Foreclosure

None of these should scare you off the channel. Each one has a mitigation, and the operators who work pre-foreclosures well just build the checks into their process:

- The seller reinstates and backs out. Get to a signed agreement before you sink real money in, and don’t count a deal until it’s under contract.

- Hidden liens and back taxes. Run a title search before closing; some liens survive foreclosure (New Funding Resources).

- Deferred maintenance. Inspect, then budget repairs honestly into your ARV math instead of hoping.

- Timeline uncertainty. Sale dates move; build slack into your plan and don’t overcommit on close dates.

- Lender delays on short sales. Expect weeks to months, and don’t spend the profit before the lender says yes (Nolo).

- Emotional sellers. Tact and honesty aren’t just decent, they’re what get the deal to the table and keep it there.

The pattern is the same across all six: verify, budget, and don’t treat a maybe like a yes.

Is Buying a Pre-Foreclosure Right for You?

Pre-foreclosure rewards a specific kind of buyer. If you have cash or flexible financing, the patience to wait out a lender, and the discipline to run title and inspections properly, this is one of the better ways to buy below retail with less competition.

It’s a poor fit if you’re on a tight clock and need a turnkey home to move into next month. The timelines slip, short sales crawl, and some deals die at the reinstatement stage after you’ve done the work. That’s the honest tradeoff. If waiting out a short-sale lender would break your plans or your patience, this channel will frustrate you, and there’s no shame in buying on the open market instead.

Build a Channel That Brings Pre-Foreclosure Sellers to You

The investors who win this channel don’t just buy the same NOD list as everyone else and hope. They build a way for distressed sellers to find them first, so the deals come inbound. That’s the seller-situation search channel BASEO builds for cash home buyers: original pages that answer the exact questions a foreclosure, probate, or divorce seller types under stress, so your site is the one they call. One Florida cash buyer went from 3 to 28 motivated seller leads a month in nine months, same market, no extra ad spend (BASEO client data).

Frequently Asked Questions

Yes. You buy directly from the owner, who still holds title, before the home goes to auction. You negotiate a price that satisfies the mortgage payoff, or, if the owner owes more than the house is worth, through a lender-approved short sale.

It can be. You often get some discount and far less competition than the open market. But the deals run longer and carry more risk, hidden liens, lender delays, a seller who backs out. It suits patient buyers who can do their diligence properly.

It varies, and there’s no fixed discount. Price depends on the owner’s equity, the home’s condition, local demand, and how motivated the seller is. Pre-foreclosures usually sell for less of a discount than auction or bank-owned homes, because the owner still controls the sale (Zillow).

In pre-foreclosure the homeowner still owns the property, and you negotiate with them before the auction. In foreclosure the lender has taken the home or sold it at auction, so you buy from the bank or at the courthouse, usually with less time to inspect. The comparison table above breaks it down.

Before a binding contract, yes. An owner can reinstate the loan or find other financing and keep the home. Once a purchase agreement is signed, normal contract law applies to both sides. Confirm your specific protections with a real estate attorney.

Final thoughts

Pre-foreclosure means buying from a motivated owner who still holds the keys. That’s where the room to negotiate lives, and it’s also why the diligence has to be tightest: the liens, the lender, and the timeline are all yours to verify before you commit.

The buyers who close these consistently aren’t just working harder lists. They’ve built a way for distressed sellers to find them first, so acquisition doesn’t depend on out-hustling everyone for the same public records. If you want to see which seller-situation searches your market already gets, and which ones a competitor is catching, that’s what the free audit is for. Written, no call required, yours to keep.